“Fed Up” is the name of a progressive initiative that describes itself as a coalition of “community‐based organizations, labor unions, policy experts, and faith leaders…united in our call for a strong economy that works for everybody and a more transparent and democratic Federal Reserve.” Its main organizer is the Center for Popular Democracy, with support from the AFL-CIO, and the Economic Policy Institute, among others.

Fed Up has two main causes. First, it raises an important issue when it questions the current governance structure of the regional Federal Reserve Banks. Ironically, while it calls for greater diversity of backgrounds among FRB directors, Fed Up never seems to notice that FRB presidents are today the main source of diversity of thinking on the Federal Open Market Committee. Between 1995 and 2013, Dan Thornton and David Wheelock have found, “there were just two dissents by governors compared with 67 by presidents.” Since 2006 there have been zero dissents by members of the Board of Governors.

Fed Up secondly offers advice to the Federal Open Market Committee, the monetary policy body whose voting members consist of the Board of Governors plus a rotating subset of Reserve Bank presidents. It urges the FOMC to pursue a secularly more expansionary monetary policy, in the erroneous hope that this would bring greater prosperity to workers. In its wishful view “The Fed should target real wage growth that is higher than economy‐wide productivity growth, in order to combat inequality and boost workers’ share of income.”

To say that “the Fed should” do x is to imply that the Fed can do x. Regrettably, however, the Fed has no policy tool with which to target real wage growth. Nor does any agency have a tool to raise real wage growth above productivity growth. The Fed can print money faster, which generates higher inflation, but this does not sustainably increase real wages or employment. The Fed cannot improve the productivity or demand for labor by generating 4% or 5% rather than 2% inflation in the long run. (Raising inflation even further to double digits would clearly harm workers by deranging economic coordination).

Nor does faster money growth sustainably lower the real interest rate. It is an elementary proposition of monetary theory that the real interest rate is independent of monetary policy in the long run. Faster money growth only raises inflation and thereby the nominal interest rate, which is determined by the real interest rate plus the expected inflation rate. For the Fed to secure lower nominal interest rates in the long run it must lower the inflation rate, and so must pursue a less expansionary monetary policy.

In June, Fed Up organized and published a letter calling on the Fed to commit explicitly to higher inflation by raising its official inflation target above the current 2% rate. Twenty‐two professional economists signed the letter, including Nobel laureate Joseph Stiglitz; former Minneapolis Fed President Narayana Kocherlakota; and several former Obama administration economists. Prominent academic signers included Justin Wolfers, Laurence Ball, and Brad DeLong. The letter can be read in its entirety here.

The letter’s argument does not turn on the above‐mentioned confusions between nominal and real variables, or confusions between short‐run and long‐run effects of monetary policy. On the contrary, it implicitly rejects them. Its argument is more sophisticated: two percentage points in higher secular inflation, by raising the secular nominal interest rate two percentage points farther above its zero lower bound, would allow the Federal Reserve temporarily to reduce the real interest rate (the nominal rate minus the given inflation rate) by two more percentage points when it lowers the nominal rate to zero in a recession. The Fed would thereby be able to deliver more stimulus.

Kocherlakota spelled out the logic in a blog post:

The inflation target helps define how much stimulus the Fed can deliver when it lowers interest rates to zero (a boundary below which the central bank has been unwilling to go). In a higher‐inflation environment, a nominal fed funds rate of zero results in a lower real, net‐of‐anticipated‐inflation rate — the rate that economists typically see as most relevant for consumer and business decisions. If, for example, people expect inflation to be 3 percent, then a zero nominal rate translates into a negative 3 percent real rate — a full percentage point lower than the Fed could achieve if expected inflation were 2 percent. Experience suggests that the Fed could use the added ammunition.

Or as David Beckworth and Ramesh Ponuru boiled down the argument: “During a recession, central banks usually cut interest rates in order to stimulate the economy. The higher the interest rate is at the start of the recession, the more they can cut it.”

Kocherlakota conceded that “there’s also a case against raising the inflation target,” although he didn’t spell it out. He concluded: “That’s why the more important part of the letter is its call for ‘a diverse and representative commission’ to re‐examine the monetary policy framework.”

The argument has been around for years that a 4% or 5% inflation target would be better than a 2% or 0% target. Its lineage goes back at least to a 1996 paper by Akerlof, Dickens, and Perry, which emphasized wage stickiness rather than the zero lower bound. (George Akerlof, by the way, is the husband of Fed Chair Janet Yellen.) More recently Olivier Blanchard in 2010, while IMF Chief Economist, suggested with co‐authors that central banks should consider raising their inflation targets and thus nominal interest rates to create more space above the zero lower bound (hereafter ZLB). Laurence M. Ball, a co‐signer of the Fed Up letter, argued explicitly for raising the inflation target to 4% in a 2014 IMF working paper emphasizing the ZLB.

The Fed Up letter argues that the ZLB has become a more frequent constraint on policy in light of a secular fall in the equilibrium real interest rate toward zero, citing an argument to this effect by San Francisco FRB president John Williams. In the words of the letter, although a 2% inflation target “seemed to give ample leverage with which the Fed could lower real interest rates” once upon a time, zero rates for seven years after the financial crisis failed at “sparking any large acceleration of aggregate demand growth.”

The most straightforward objection to raising the inflation target is that a higher secular inflation rate raises the well‐known costs of inflation. It means a higher and more distortive tax on money‐holding, reducing consumer welfare. It means greater “menu costs” of more frequently changing nominal prices. Higher inflation rates are associated with higher variability in relative prices, increasing noise in the price system. But these costs alone are not enough to counter the claim that the welfare costs of a more frequently binding ZLB are even greater. (The letter simply dismisses the costs of increasing the inflation rate by few percentage points, asserting a “lack of evidence that moderately higher inflation would harm Americans’ standard of living.”)

An effective challenge to the proposal for a higher inflation target requires a challenge to the underlying claim that the ZLB prevents an effective anti‐recession monetary policy. The underlying claim rests on the New Keynesian or Taylor Rule conception that monetary policy is recession‐fighting if and only if it lowers the nominal interest rate. But this is a mistake. The problem of recession, to the extent that monetary policy can relieve it, is an unsatisfied excess demand to hold money (the quantity demanded exceeds the quantity supplied at the current price level and nominal interest rate). Sales and employment are depressed because an excess demand for money corresponds to an excess supply of goods and services in general: consumers don’t buy when they are trying to build up their money balances. Monetary policy can in principle remedy the problem by expanding the quantity of money in the right amount at the right time.

But wait, you might say, didn’t quantitative easing fail to improve anything in the last recession? No. In the relevant sense – increasing the quantity of money in the hands of the public – quantitative easing wasn’t even tried. As I have emphasized in a previous article, in the face of a large 2009 increase in the holding of M2 balances relative to income (a large drop in the velocity of M2), the Fed did not raise the path of M2 growth. Its QE programs did raise the path of M0, the monetary base, but the Fed prevented that M0 growth from fueling faster M2 growth by paying banks to sequester the additional M0 (it paid them interest on excess reserves for the first time).

Absent offsetting higher interest on excess reserves, quantitative easing is capable in principle of providing all the monetary “looseness” needed. The ZLB is no obstacle to expanding M2. Consequently a higher secular inflation rate brings with it higher costs, but no offsetting benefit of enlarging the power of monetary policy to do the needful in a recession.

Finally, it should be noted that Chair Yellen, after having rejected the idea of raising the Fed’s inflation target on many previous occasions as a threat to the credibility of the FOMC, responded more positively to the idea after the Fed Up letter. At her June 14 press conference, she echoed the letter’s argument:

[A]ssessments of the level of the neutral likely level currently and going forward of the neutral Federal funds rate have changed, and are quite a bit lower than they stood in 2012 or earlier years. That means that the economy is, has the potential where policy could be constrained by the zero lower bound more frequently than at the time that we adopted our 2% objective. So it’s that recognition that causes people to think we might be better off with a higher inflation objective. That is an important set, this is one of our most critical decisions and one we are attentive to evidence and outside thinking. It’s one that we will be reconsidering at some future time. And it’s important for our decisions to be informed by a wide range of views and research, which is ongoing inside and outside the Fed.

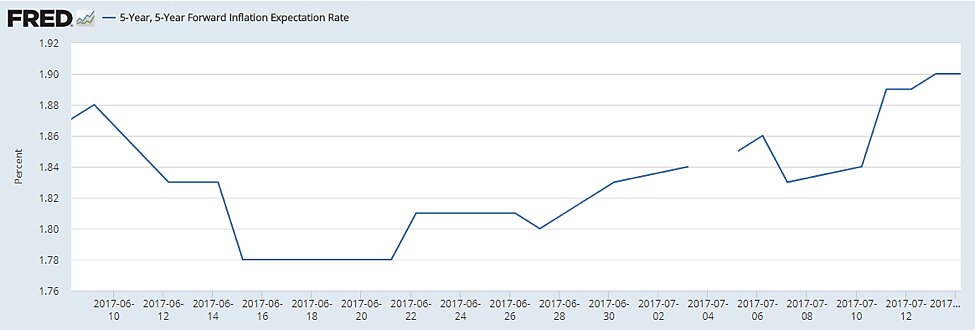

The day after Yellen’s press conference, as the below chart shows, a leading market measure of the expected inflation rate stopped falling. It has since risen, and is now 12 basis points higher.